Interesting article on how Nigeria’s Naira has struggled against the dollar since the 80s. Read below:

Since 1986, the Nigerian naira’s relationship with the US dollar (and other foreign currencies) has been erratic, (un)predictable, violent and full of heartbreak and tears. The built-in dysfunction has also made a lot of people very rich.

This piece seeks to trace the history of how Nigeria’s foreign exchange management became what it is to the point where the exchange rate of the naira has become a deeply political matter.

The current debate continues to be around whether or not Nigeria should devalue the naira. But what if devaluation is the answer to a non-existent question?

President Ibrahim Babaginda’s Second-Tier Foreign Exchange Market (SFEM)

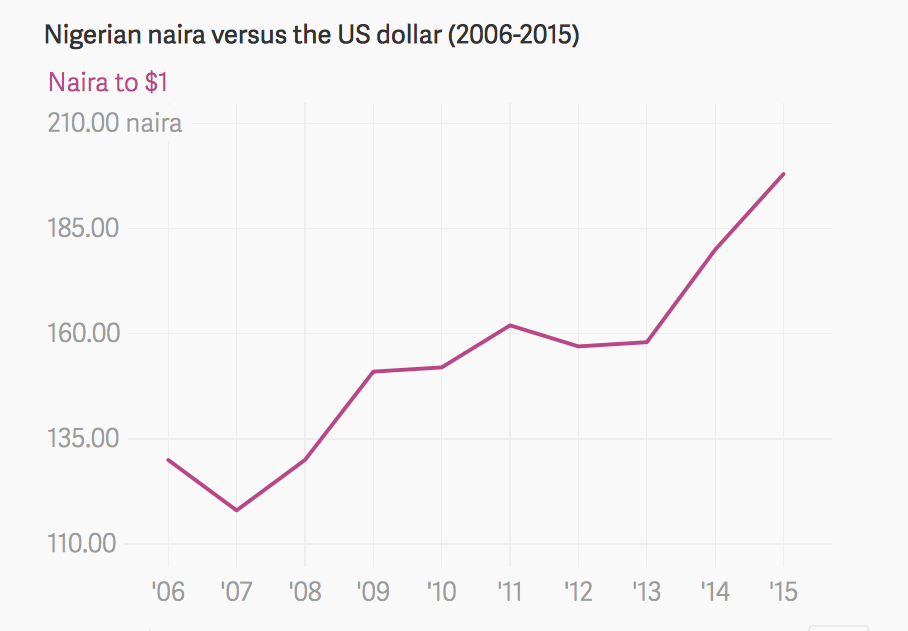

In September 1986, the SFEM was introduced as part of a package of IMF reforms that general Babangida was forced to accept given the mess that Nigeria had managed to find itself. Before this, the naira exchanged for something like 90 kobo to $1. By the time IBB left office in 1993, the naira was exchanging for 17 naira to $1. It was during this time that Bureau de Change were introduced into the economy.

The rate at which the naira depreciated in those few years probably explains why Nigerians have never gotten over the idea of a strong currency as the mark of a ‘strong’ economy. People only remember that things got worse as the naira lost ground to the dollar. To make matters worse, the industrialisation that a weaker exchange was supposed to bring about never materialised.

President Sani Abacha (1993-1998)

From the day that Abacha took power to the day he died on June 8 1998, a period of five years, the ‘official’ exchange rate of the naira to the dollar never changed from 22 naira to $1. The Autonomous Foreign Exchange Market (AFEM) was introduced in 1995 as a way for the Central Bank of Nigeria (CBN) to sell forex to end users at ‘market’ rates.

But it is one thing to declare that the naira is worth 22 naira to $1. It is quite another thing to be able to satisfy all the people who will demand to buy dollars at that price. Given that oil prices were below $20 a barrel in this period, there was a very limited amount of dollars available (whatever was left after those in charge had helped themselves).

This rigid exchange rate gave birth to a phenomenon that is now a permanent fixture today — the mainstreaming of the forex black market. At one point, the naira was trading as high as 88 naira to $1 while the official rate remained at 22 naira. Bankers came up with what they used to call the ‘blended’ rate. Say a client requested $1 million from their bank, the bank would inflate it to say $10 million and then take the request to AFEM knowing that CBN would never approve the full request anyway. Whatever was obtained from CBN was then ‘blended’ with the rest obtained from the black market.

It does not take a genius to know that if the black market rate was four times the official rate, people made an absolute fortune from the arbitrage. A lot of banking fortunes that remain to this day in Nigeria were made in this period. It was sweet business.

Joseph Sanusi (CBN governor 1999 to 2004)

The Interbank Foreign Exchange Market (IFEM) was introduced under Joseph Sanusi. Given how Nigeria’s reserves had been depleted severely in the two years before he took over, the naira was never going to survive the ‘military fiction’ rate of 22 naira for very long. Within a year, the naira was trading at 85 naira but this time, the gap with the black market had closed considerably at 105 naira to the $1—particularly if compared to what happened under president Abacha.

In addition to low oil prices, Nigeria was also struggling to service its $33 billion foreign debt which was eating up valuable foreign exchange.

All the things we see today were also experimented with under Sanusi. He suspended the IFEM for six months when the naira came under pressure and also introduced a limit to the margin (above CBN’s rate) that banks could sell their own forex for. Current governor Godwin Emefiele is doing the same thing today.

Again, the attempt to ‘control’ the exchange rate gave rise to all sorts of funny games. Since the rate at which banks could sell their forex was fixed, they simply complied with this rate at the IFEM but then collected an extra payment outside the system to make up the difference with the ‘real rate’ at which they were actually selling. Some bankers called this game ‘NIBSS and Drafts’ i.e. you pay the official rate via NIBSS (Nigeria Inter-bank Settlement System) but settle the difference with a bank draft.

Forex round tripping games flourished. Nigeria had all sorts of banks which totalled around 90 at one point. The licences were cheap and you could make the cost of the licence back in one year from round tripping. It was a win-win business. Banks also set up foreign entities which they used to help their clients move money abroad. One bank, now defunct, used to regularly reward employees with a Volkswagen Jetta for outstanding performance. In banking circles, the joke then was that the Jetta was always won by the bankers in the treasury department i.e. the best round trippers in the bank.

Chukwuma Soludo (2004-2009) and The Oil Boom

Starting in late 2003, oil prices began to rise steadily from around $30 per barrel till they peaked at $140 per barrel in the middle of 2008. It was also during this period of rising oil prices that Nigeria obtained its $18 billion debt relief from the Paris Club. It was like being in heaven.

First of all, rising oil prices allowed Nigeria’s foreign reserves to increase substantially. There were reserves and there was also the Excess Crude Account (ECA) which had more than $20 billion at one point in 2008.

What these happy events allowed governor Soludo do was to harmonise the four different exchange rates at the time — CBN, Interbank, Bureau de Change and wire rates. He did this by liberalising the foreign exchange manual and including all sorts of things that were previously not accepted as valid for foreign exchange requests. For example, previously you could only obtain foreign exchange to bring in ‘raw materials’. But in the world we now live in, manufacturing has changed to the point where you might need to import some finished products to add to your own process. His liberalisation recognised this.

He also made things like medical bills and even credit card bills allowable. And he achieved his aim. In a short while, the different rates converged to within one naira of each other given that there was no need to go to the black market or bureaux de change to get forex when you could get it officially from your bank. Nigeria was awash with dollars and bankers at the time spoke of not even needing to go to CBN for dollars for weeks. Indeed, they say CBN staff used to harass them as to why they had not come to buy dollars. This was the period when the naira gained about 20% against the dollar without anyone explicitly trying to ‘strengthen’ it.

And then the inevitable happened — oil prices started to fall from late 2008 to less than $50 by the end of the year. But this time around, Nigeria was in a pretty good position to weather the storm with reserves totalling around $62 billion. Nevertheless, Soludo engineered some kind of artificial scarcity of forex to allow a devaluation of the naira. He also banned the Interbank market for six months.

All told, when Soludo took office, the naira was trading at 127 naira to $1 and by the time he left in 2009, it was around the 147 naira mark. But this masks the fact that in 2008, it actually went as low as 115 naira to $1 at one point. Oil prices started to recover pretty quickly and so if Soludo had done nothing, it would have just cost Nigeria some of its reserves and normal service would have resumed after about eight months. But the temptation to ‘do something’ is always strong.

Sanusi Lamido Sanusi (June 2009-Feb 2014)

As soon as oil prices recovered, Central Bank governor Sanusi Lamido Sanusi (SLS) restored the Interbank and WDAS markets that Soludo had previously banned. But he then faced a somewhat strange problem later on. Oil prices were high but Nigeria was not building up its reserves for reasons that are perhaps now obvious. This meant that he did not have enough dollars to defend the naira and keep it stable as he wanted.

To solve this problem, he removed the one-year restriction on foreign investors who wanted to buy government bonds. (Previously, any foreign investor who wanted to buy Nigerian government bonds needed to hold the bonds for one year). The dollars came pouring in. But then this was what is known as ‘hot money’ i.e since you did not need to hold the investment for one year, the money poured in and out rapidly.

JP Morgan’s requirement to include Nigeria in its index was always that the market was kept liquid. As soon as this was done with the removal of the restriction, there was not much else standing in the way of Nigeria being included in the index. Nigeria’s Debt Management Office even took a 2-page advert in the newspapers congratulating President Jonathan on Nigeria’s inclusion in the JP Morgan Index.

Given that oil prices remained high throughout SLS time in office, some measure of stability was achieved. The naira was trading at 148 naira to the dollar when he took office in 2009 and was 164 naira by the time he was suspended from office in February 2014. The stability of the graveyard.

Godwin Emefiele and where we are today

It costs something like $30 to extract a barrel of crude oil in Nigeria. So when oil was trading at $110 Nigeria had a margin of around $80 to play with. But when oil drops to $45 as it has now, that $80 margin turns to $15 as the cost of getting the oil out of the ground still has to be incurred.

To put the above numbers another way — while oil prices have dropped by 60%, the revenues available to Nigeria have dropped by 81%. That is, revenues have dropped much more than oil prices have dropped. Nigeria is earning almost nothing these days and you can imagine how disastrous it will be if oil prices drop further to $40 or even less.

When things like these happen, one way to defend yourself is by unleashing your reserves. So for example, Algeria had something like $150 billion in reserves when the oil crisis hit. But as stated above, Nigeria did not save anything when the going was good so the country walked into this oil price crash practically naked. Reserves are allegedly $30 billion today but in reality they are much less (maybe around $20 billion when you account for all the money that is already ‘spoken for’)

Governor Emefiele has done the usual in response. He has banned the Interbank forex market and also banned 41 items from being eligible for forex, directly undoing what Soludo did. Forex is now essentially being rationed and the CBN is deciding who gets what and how much. Rumours of privileged people making a fortune from the confusion and arbitrage are circulating among bankers once again.

What can we learn from all this? The most obvious lesson here is that Nigeria has never quite figured out how to spend oil money. When prices are high, you save as much as you can. When prices fall, you open the tap and increase your spending. The point of this is to keep things going steady and avoid wild shocks in the economy.

What Nigeria instead does is to increase spending once oil prices go up with things like increased minimum wages, bloating the civil service or even outright theft. Politics always manages to bully economics. With the exception of the one time under Soludo, this is how things have always been — Nigeria is never ready for when oil prices drop. And yet, oil prices dropping is as sure to happen as night following day.

The moment oil prices crash, businesses and transactions that were perfectly legal suddenly become ‘unpatriotic’.

Another lesson is that the politicisation of the exchange rate of the naira is an unhealthy obsession in Nigeria. It gives politicians an incentive to wage war against reality by doing things that are economically harmful in the name of maintaining a ‘strong’ currency. Economic nationalism comes into fashion — why do we need to import rice when we can grow it here?!

Yet, the rhetoric only lasts till oil prices go back up and then politicians can return to their old ways.

The very act of trying to fiddle with the currency whenever we run into trouble is what really needs to be looked at. The moment oil prices crash, businesses and transactions that were perfectly legal suddenly become ‘unpatriotic’. And then a pointless argument about what should be imported and what should not predictably take up valuable media space.

Nigeria wants to have high oil prices and spend without saving. It then wants to keep its exchange rate ‘stable’ even when revenues have collapsed dramatically.

It is not possible to have all these things at the same time. It’s time to depoliticise the naira exchange rate by allowing the market to determine its fair value.

There are no easy answers to this problem. Having an economy that is not tied to the price of one product that is bound to have wild price swings is an obvious solution. But wanting a diversified economy and actually having one are two completely different things. And if Nigeria is going to diversify its economy, it has not even started yet.

Over the last 20 years or so, Nigeria has slowly but steadily moved towards a market-determined foreign exchange system. This is the right thing to do as it takes the matter out of the hands of politicians. Given the severity of the current crisis, all those gains are now being undone with all kinds controls and erratic moves that slowly choke the life out of the economy.

If Nigeria won’t save when oil prices are high, then allowing the naira to float and be determined by the market is the only credible option left. Who knows, this might even teach some sense.

God save our Naira and Naija…